On May 15, 2024, FINMA unveiled amendments to the Financial Services Act (FinSA) and the Financial Institutions Act (FinIA), focusing on behavioural duties for financial service providers. The key points relevant for wealth managers are:

Providers, including wealth managers, must provide accurate, comprehensive information to clients, ensure the suitability of recommendations, and disclose potential risks. This includes:

a) Clarifying the level of advice (transactional vs. portfolio-based) when establishing the mandate agreement.

b) Providing information about complex leveraged products like CFDs and other highly leveraged products.

c) Disclosing concentration risks if a portfolio exceeds 10% in an instrument (excluding diversified funds) or 20% in an issuer.

Prioritising clients’ best interests is paramount. Wealth managers must tailor services to each client’s individual needs, preferences, and risk tolerance. This involves:

a) Assessing clients’ knowledge and experience in relevant asset classes.

b) Obtaining detailed information about clients’ overall financial situations (e.g., entire “balance sheet,” not just net values) for accurate risk profiling.

Transparency remains central. Providers must disclose all relevant information, including potential conflicts of interest arising from in-house or external financial products.

To mitigate conflicts of interest and preserve independence, providers must clearly disclose inducements (commissions, rebates, or incentives) that could impair their duty to act in clients’ best interests.

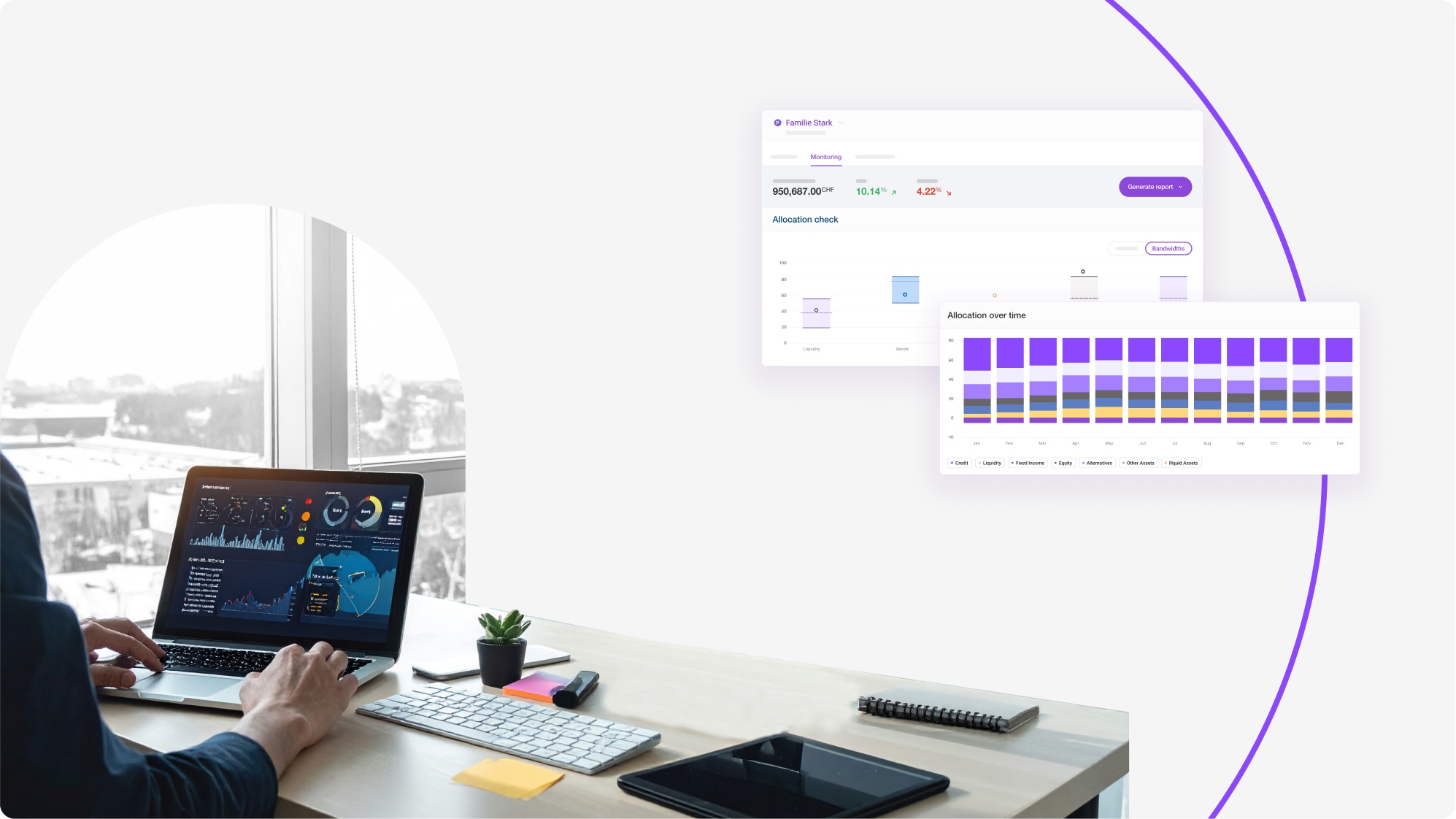

Our Wealth Discover application offers wealth managers embracing FINMA’s new behavioural duties several advantages.

Wealth managers can strengthen trust and credibility with clients by sharing access to Wealth Discovery for Investors. Etops clients can easily adhere to the enhanced information duty by providing their wealth clients monitoring capabilities for bulk risks, asset allocation checks, and product risks.

Compliance with the updated regulations can serve as a competitive differentiator, positioning wealth managers as trusted advisors committed to investor protection and finding the best-suited strategies for their client’s situations. By having an integrated behavioral profiling tool, we offer a state-of-the-art profiler that includes all the latest regulatory guidelines from day one.

Staying ahead of upcoming regulatory changes and evolving client servicing needs requires a continuously improving SaaS product. Wealth Discovery is built from the ground up to scale across wealth management and adapt to evolving needs, with frequent updates and enhancements.

As we navigate the implications of FINMA’s new behavioral duties (planned for beginning of 2025), Etops is monitoring the landscape and assessing how we can help our platform users navigate the rules more easily. We are dedicated to building software that helps you make better decisions, stay compliant and provide better services to your clients.

For further insights and updates on regulatory developments, stay connected with Etops through our website and social media channels.