Traditional advisory models are built on client segments, risk categories, and standardized allocation frameworks. This approach has proven efficient, yet it remains inherently generic. The more homogeneous the model, the weaker the true differentiation in the market.

Hyper-personalization shifts the focus from segments to the client’s individual wealth reality. Investment strategies are no longer defined by averages, but by concrete objectives, liquidity needs, tax considerations, sustainability preferences, and existing asset structures. Advisory services are not becoming more complicated, they are becoming more precise.

For wealth managers, the implication is clear: standardization drives efficiency. Individualization drives differentiation.

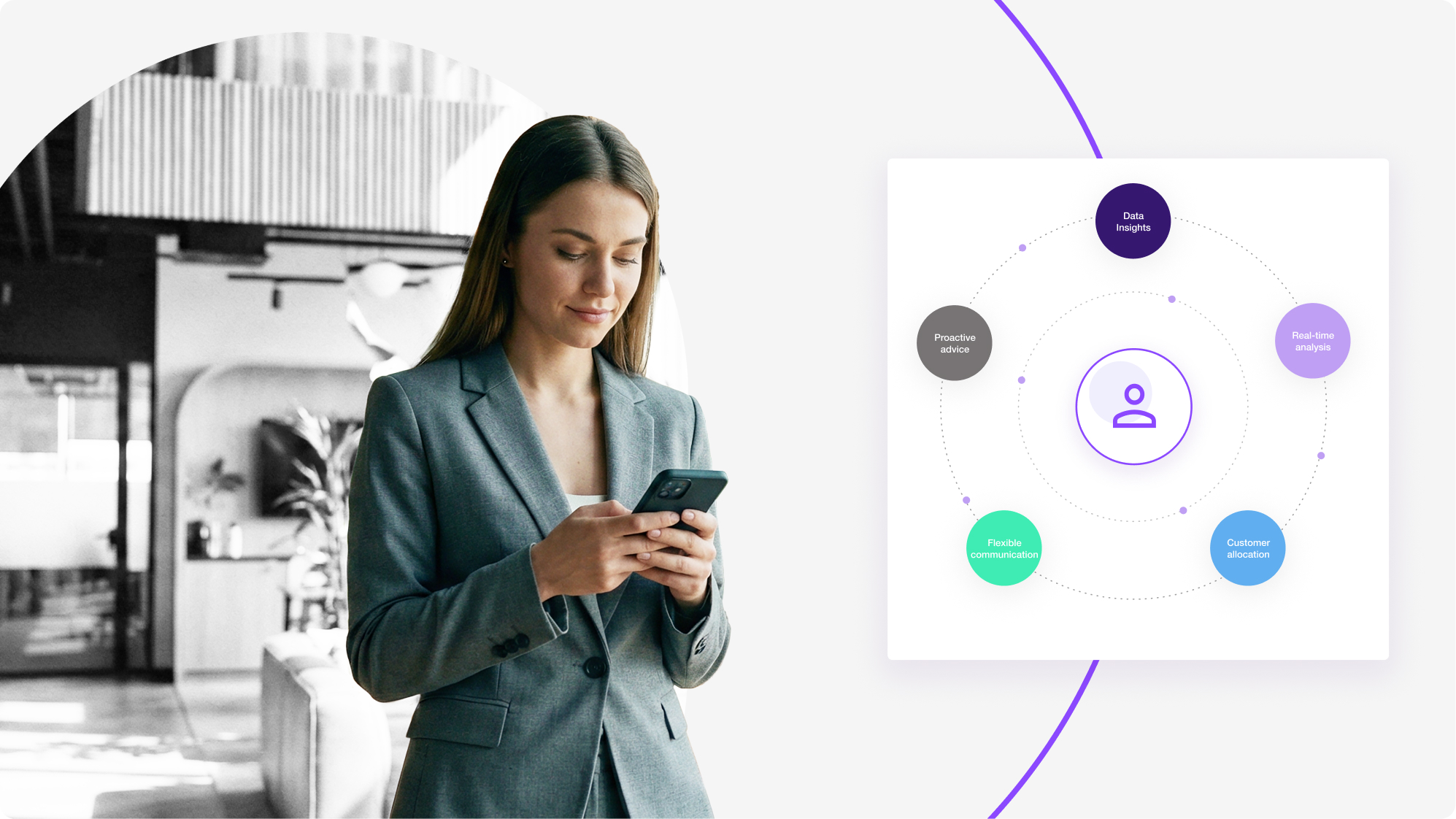

True individualization does not begin in the client meeting, it begins within the data architecture. Without a consolidated, structured, and analyzable data foundation, personalization remains fragmented.

Hyper-personalization depends on integrated data intelligence. Portfolio, market, and client data are systematically aggregated and transformed into actionable insights, creating decision frameworks that go beyond static risk profiles to reflect the actual composition of a client’s wealth.

In this context, technology is not an add-on, it is a prerequisite for scalability. Only when analytics, reporting, and process logic are integrated can personalization be implemented sustainably and economically.

Traditional advisory models respond to market movements or client inquiries. Hyper-personalization enables a fundamentally different approach: forward-looking wealth steering grounded in data-driven analysis.

Risks, concentration exposures, and opportunities are identified early, allowing advisors to derive tailored recommendations aligned with each client’s specific portfolio situation. Client conversations gain substance because they are anchored in the concrete impact on the individual mandate, not in general market commentary.

The decisive value lies in relevance. Recommendations are transparent, well-founded, and directly connected to the client’s financial reality.

Competition in wealth management continues to intensify. Investment products are increasingly comparable, and margins remain under pressure. Differentiation no longer stems primarily from product offerings, but from advisory quality and client experience.

Hyper-personalization strengthens this lever. It enhances transparency, improves decision quality, and deepens long-term client relationships. At the same time, it enables operational efficiency, standardized processes run in the background while the advisory experience remains fully individualized.

Institutions that embed this approach strategically position themselves not as product providers, but as long-term partners in wealth stewardship.

Hyper-personalization is not an optional innovation. It is a structural response to evolving client expectations and growing competitive pressure. Firms that systematically combine data intelligence, analytics, and advisory expertise create sustainable differentiation. In wealth management, future success will be defined not only by performance, but by relevance.